Please select your location and the type of investor you are so we can share the most relevant information with you.

For Institutional / Wholesale / Professional Clients

The content on this website is intended for institutional and professional investors in the United States only and is not suitable for individual investors or non-U.S. entities. Institutional and professional investors include pension funds, investment companies registered under the Investment Company Act of 1940, financial intermediaries, consultants, endowments and foundations, and investment advisors registered under the Investment Advisors Act of 1940.

TERMS AND CONDITIONS OF USE

Please read the information below. By accessing this web site of Thornburg Investment Management, Inc. ("Thornburg" or "we"), you acknowledge that you understand and accept the following terms and conditions of use.

Disclaimers

Products or services mentioned on this site are subject to legal and regulatory requirements in applicable jurisdictions and may not be licensed or available in all jurisdictions and there may be restrictions or limitations to whom this information may be made available. Unless otherwise indicated, no regulator or government authority has reviewed the information or the merits of the products and services referenced herein. Past performance is not a reliable indicator of future performance. Investments carry risks, including possible loss of principal.

Reference to a fund or security anywhere on this website is not a recommendation to buy, sell or hold that or any other security. The information is not a complete analysis of every material fact concerning any market, industry, or investment, nor is it intended to predict the performance of any investment or market.

All opinions and estimates included on this website constitute judgements of Thornburg as at the date of this website and are subject to change without notice.

All information and contents of this website are furnished "as is." Data has been obtained from sources considered reliable, but Thornburg makes no representation as to the completeness or accuracy of such information and has no obligation to provide updates or changes. Thornburg disclaims, to the fullest extent of the law, any implied or express warranty of any kind, including without limitation the implied warranties of merchantability, fitness for a particular purpose and non-infringement.

If you live in a state that does not allow disclaimers of implied warranties, our disclaimer may not apply to you.

Although Thornburg intends the information contained in this website to be accurate and reliable, errors sometimes occur. Thornburg does not warrant that the information to be free of errors, that the functions contained in the site will be uninterrupted, that defects will be corrected or that the site and servers are free from viruses or other harmful components. You agree that you are responsible for the means you use to access this website and understand that your hardware, software, the Internet, your Internet service provider, and other third parties involved in connecting you to our website may not perform as intended or desired. We also disclaim responsibility for damages third parties may cause to you through the use of this website, whether intentional or unintentional. For example, you understand that hackers could breach our security procedures, and that we will not be responsible for any related damages.

Thornburg Investment Management, Inc. is regulated by the U.S. Securities and Exchange under U.S. laws which may differ materially from laws in other jurisdictions.

Online Privacy and Cookie Policy

Please review our Online Privacy and Cookie Policy, which is hereby incorporated by reference as part of these terms and conditions.

Third Party Content

Certain website's content has been obtained from sources that Thornburg believes to be reliable as of the date presented but Thornburg cannot guarantee the accuracy, timeliness, completeness, or suitability for use of such content. The content does not take into account individual investor's circumstances, objectives or needs. The content is not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services, nor does it constitute investment advice and should not be used as the basis for any investment decision.

Suitability

No determination has been made regarding the suitability of any securities, financial instruments or strategies for any investor. The website's content is provided on the basis and subject to the explanations, caveats and warnings set out in this notice and elsewhere herein. The website's content does not purport to provide any legal, tax or accounting advice. Any discussion of risk management is intended to describe Thornburg's efforts to monitor and manage risk but does not imply low risk.

Limited License and Restrictions on Use

Except as otherwise stated in these terms of use or as expressly authorized by Thornburg in writing, you may not:

Modify, copy, distribute, transmit, post, display, perform, reproduce, publish, broadcast, license, create derivative works from, transfer, sell, or exploit any reports, data, information, content, software, RSS and podcast feeds, products, services, or other materials (collectively, "Materials") on, generated by or obtained from this website, whether through links or otherwise;

Redeliver any page, text, image or Materials on this website using "framing" or other technology;

Engage in any conduct that could damage, disable, or overburden (i) this website, (ii) any Materials or services provided through this website, or (iii) any systems, networks, servers, or accounts related to this website, including without limitation, using devices or software that provide repeated automated access to this website, other than those made generally available by Thornburg;

Probe, scan, or test the vulnerability of any Materials, services, systems, networks, servers, or accounts related to this website or attempt to gain unauthorized access to Materials, services, systems, networks, servers, or accounts connected or associated with this website through hacking, password or data mining, or any other means of circumventing any access-limiting, user authentication or security device of any Materials, services, systems, networks, servers, or accounts related to this website; or

Modify, copy, obscure, remove or display the Thornburg name, logo, trademarks, notices or images without Thornburg's express written permission. To obtain such permission, you may e-mail us at info@thornburg.com.

Severability, Governing Law

Failure by Thornburg to enforce any provision(s) of these terms and conditions shall not be construed as a waiver of any provision or right. This website is controlled and operated by Thornburg from its offices in Santa Fe, New Mexico. The laws of the State of New Mexico govern these terms and conditions. If you take legal action relating to these terms and conditions, you agree to file such action only in state or federal court in New Mexico and you consent and submit to the personal jurisdiction of those courts for the purposes of litigating any such action.

Termination

You acknowledge and agree that Thornburg may restrict, suspend or terminate these terms and conditions or your access to, and use, of the all or any part this website, including any links to third-party sites, at any time, with or without cause, including but not limited to any breach of these terms and conditions, in Thornburg's absolute discretion and without prior notice or liability.

Please read through all of the Terms and Conditions of Use above to continue.

Region

Americas

Asia Pacific

Europe

Rest of the World

Agree & Continue

Unsubscribe

Confirm you would like to unsubscribe from this list

Unsaved Changes

You have unsaved changes on the page. Would you like to save them?

Remove strategy

Confirm you would like to remove this strategy from your list

Overall Morningstar Rating among 193 Global Moderately Aggressive Allocation funds, based on risk-adjusted returns for class I shares, using a weighted average of the funds three-, five-, and ten-year ratings: respectively, 5 stars, 5 stars and 4 stars among 193, 181 and 148 funds, as of 30 Jun 2025.

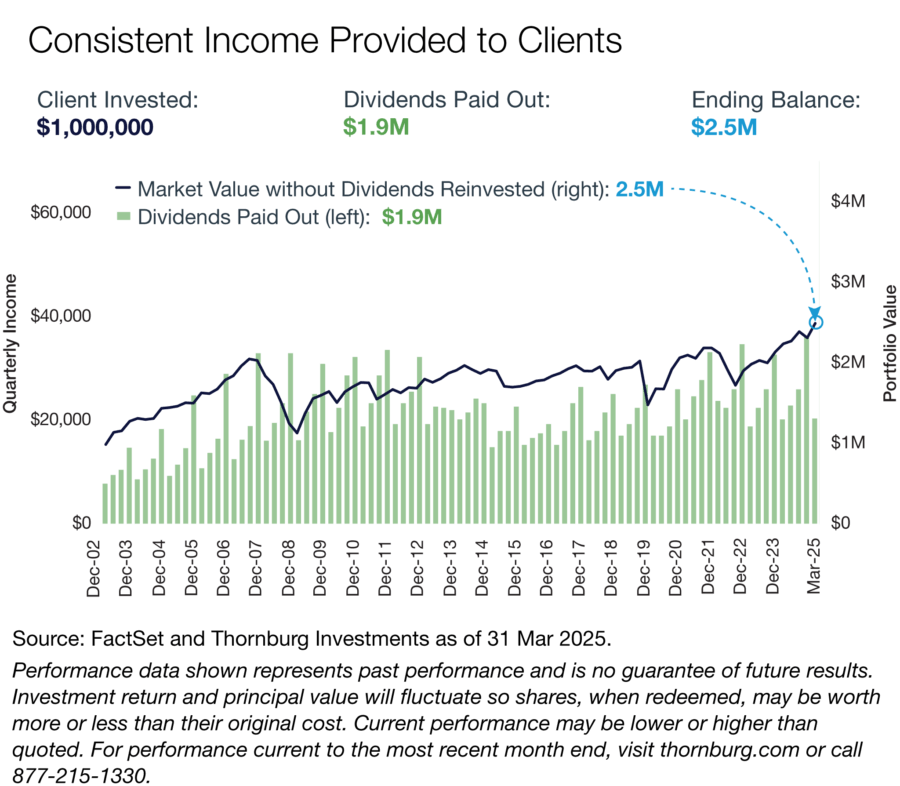

Global, diversified multi-asset portfolio of income-producing stocks and bonds that seeks to deliver an attractive and growing income stream.

Proven bottom-up fundamental research process to identify dividend-paying companies with strong cash flows that have both the ability and willingness to pay and grow their dividends over time.

Highly active, flexible approach that allows us to go anywhere in the world to seek income.

Investment Objective

The fund’s goal is to provide investors with a level of current income which exceeds the average yield on U.S. stocks generally, and which will grow, subject to periodic fluctuations, over the years on a per share basis.

Investment Approach

The strategy is a multi-asset portfolio of global dividend-paying stocks selected via a bottom-up, fundamentals and valuation-sensitive process. The strategy seeks to generate an attractive and growing income stream, with capital appreciation over time by building a portfolio of companies that have the ability and willingness to generate cash flow and distribute dividends to its shareholders.

Thornburg Investment Income Builder Fund's Blended Index is composed of 25% Bloomberg U.S. Aggregate Total Return Value USD and 75% MSCI World Net Total Return USD Index, rebalanced monthly.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate so shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than quoted.

The maximum sales charge for the equity funds' A shares is 4.50%. C shares include a 1% contingent deferred sales charge (CDSC) for the first year only. There is no up-front sales charge for class I or R shares.

Morningstar quartile ranking for Global Moderately Aggressive Allocation category is based on total returns before sales charges.

Prior to inception of I and R share classes, performance is hypothetical and was calculated from actual returns of an earlier share class adjusted for the expenses of the newer share class.

Share class inception dates: A shares, 24 Dec 2002; C shares, 24 Dec 2002; I shares, 3 Nov 2003; R3 shares, 1 Feb 2005; R4 shares, 1 Feb 2008; R5 shares, 1 Feb 2007; R6 shares, 10 Apr 2017.

Fund Fees

Fund Fees

(As of 1 Feb 2025)

Gross Expense Ratio (%)

0.93

Net Expense Ratio (%)

0.93

Expense Ratios - Expressed as a percentage of total fund assets and include management fees and operating costs. Expense ratios fluctuate over time and the expense ratio in the prospectus may differ from the actual expense ratio. The fund's total return includes the deduction of expenses.

For more detailed information on fund expenses, please see the fund's prospectus.

The Hypothetical Growth graph compares a hypothetical investment in the Fund to the performance of the Index for the stated time period. Returns reflect reinvestment of dividends and capital gains, if any, as well as all fees and expenses.

Sector, Industry, and Market Capitalization are based on the portfolio's equity holdings. Credit Quality and Maturity are based on the portfolio’s fixed income holdings. Geography and Asset Class are based on the full portfolio.

Credit quality ratings use the highest rating available from either S&P Global Ratings or Moody's Investors Service. Unrated securities are evaluated by the firm using available data and their own analysis that may be similar to that of a nationally recognized rating agency; however, such determination is not equivalent to a national agency credit rating. "NR" = Not Rated.

Holdings with the Geography breakdown are classified by country of risk as determined by MSCI and Bloomberg.

Cash includes cash and cash equivalents. Weights are percentages of total portfolio unless otherwise noted.

The percentages may not add up to 100 due to rounding.

Portfolio Managers

Portfolio Managers

Matt Burdett

Head of Equities and Managing Director

Matt Burdett is head of equities and a portfolio manager for Thornburg Investment Management. He rejoined the firm in 2015 as an associate portfolio manager. Matt was named a managing director and was promoted to portfolio manager in 2018 and to head of equities in 2024. Matt spent several years as a senior vice president and portfolio manager at PIMCO,…

Vice Chairman, Chief Investment Strategist and Managing Director

Brian McMahon is chief investment strategist for Thornburg Investment Management. Brian is deeply respected for his market and investment insight and serves as a key voice for the investment team and Thornburg clients. He also co-manages Thornburg’s global equity portfolios and serves as vice chairman of Thornburg. Brian joined Thornburg in 1984 as chief investment officer; a role he held…

Christian Hoffmann is head of fixed income and a portfolio manager for Thornburg Investment Management. He joined the firm in 2012 as a fixed income analyst and was promoted to associate portfolio manager in 2014. Christian was named a managing director in 2017, was promoted to portfolio manager in 2018, and to head of fixed income in 2024. Prior to…

This communication is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

Investments carry risks, including possible loss of principal. Additional risks may be associated with investments outside the United States, especially in emerging markets, including currency fluctuations, illiquidity, volatility, and political and economic risks. Investments in small- and mid-capitalization companies may increase the risk of greater price fluctuations. Portfolios investing in bonds have the same interest rate, inflation, and credit risks that are associated with the underlying bonds. The value of bonds will fluctuate relative to changes in interest rates, decreasing when interest rates rise. Investments in the Fund are not FDIC insured, nor are they bank deposits or guaranteed by a bank or any other entity.

The performance of any index is not indicative of the performance of any particular investment. Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. Investors may not make direct investments into any index.

Diversification does not assure or guarantee better performance and cannot eliminate the risk of investment losses.

Neither the payment of, or increase in, dividends is guaranteed.

A bond credit rating assesses the financial ability of a debt issuer to make timely payments of principal and interest. Ratings of AAA (the highest), AA, A, and BBB are investment-grade quality. Ratings of BB, B, CCC, CC, C and D (the lowest) are considered below investment grade, speculative grade, or junk bonds.

Credit quality ratings for Thornburg Investment Income Builder used ratings from Moody's Investors Service. Where Moody's ratings are not available, we have used S&P Global Ratings. Where neither rating is available, we have used ratings from other nationally recognized statistical rating organizations (NRSROs).

Class R shares are limited to retirement platforms only.

Class I shares may not be available to all investors. Minimum investments for the I share class may be higher than those for other classes.

There is no guarantee that the Fund will meet its investment objectives.

To determine a fund's Morningstar Rating™, funds and other managed products with at least a three-year history are ranked in their categories by their Morningstar Risk-Adjusted Return scores. The top 10% receive 5 stars; the next 22.5%, 4 stars; the middle 35%, 3 stars; the next 22.5%, 2 stars; and the bottom 10% receive 1 star. The Risk-Adjusted Return accounts for variation in a managed product's monthly excess performance (excluding sales charges), placing more emphasis on downward variations and rewarding consistent performance. Other share classes may have different performance characteristics.

Please see our glossary for a definition of terms.

Thornburg mutual funds are distributed by Thornburg Securities LLC.

Thornburg Investment Management, Inc. mutual funds are sold through investment professionals including investment advisors, brokerage firms, bank trust departments, trust companies and certain other financial intermediaries. Thornburg Securities LLC (TSL) does not act as broker of record for investors.

“Bloomberg®” and the Bloomberg index(es) mentioned in this piece are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by Thornburg Investment Management. Bloomberg is not affiliated with Thornburg, and Bloomberg does not approve, endorse, review, or recommend Thornburg. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to Thornburg.

Our investment professionals travel the world to evaluate global markets and unearth the most optimal ideas. Josh Rubin recently visited the United Arab Emirates (UAE), and here are his perspectives.

Our investment professionals travel the world to evaluate global markets and unearth the most optimal ideas. Josh Rubin recently visited India, and here are his perspectives.

Cookies Preference Center

Strictly Necessary Cookies

Whilst these cookies cannot be turned off (as they are needed to run our website securely), they do not store any personal data about you. If you are reluctant to accept use of them, we advise you navigate away from this website.

Statistics Cookies

These cookies gather information about how you use our website, for example which pages you visit most often. The information collected is completely anonymous and used only for the purpose of improving user experience for our website visitors.

Marketing Cookies

These cookies gather information about your browsing habits and allow us to better understand your interests. They remember that you've visited our website and share this information with our partners, such as advertisers.

Preferences Cookies

These cookies allow our website to remember the choices you make (such as language or location selection) and tailor the experience to provide enhanced features and relevant content for you.