Over many years, ETF capital market teams have talked about how to execute ETFs, but there is limited insight into the “Why?” We seek to clarify not only how to execute ETF trades but also the rationale behind best practices.

Timing of Trades: Avoid Trading at the Market Open or Close

At the market open…

At market open, bid-ask spreads are typically wider as market makers process overnight news. Spreads usually normalize 10–15 minutes after opening.

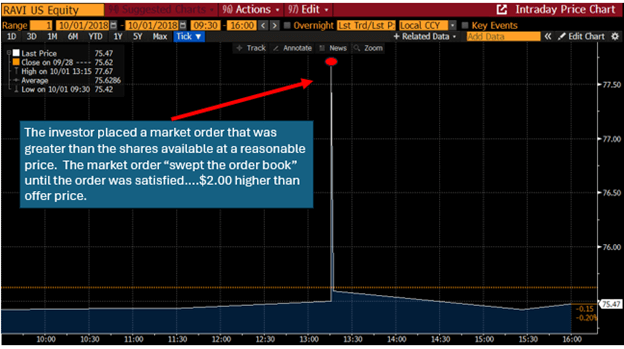

Time Matters…for lower volume ETFs

At the market open (9:30 a.m. EST), regulation requires market makers to have two-sided continuous quotes that are up to 20% wide. This regulatory band narrows to 8% at 9:40 am EST. At 9:40 am EST, market-making systems hit the ‘tighten it up’ button and presented a significantly improved quotation. It doesn’t mean that all quotes are 20% wide at 9:30 am, but low and mid-volume ETFs tend to have wider markets. Pausing for about 10-15 minutes allows these products to settle in.

Another nuanced reason – Reg Sho requires market makers to be flat or long their short ETF position within two days after settlement. This was the SEC’s method to force timely share delivery. For low- or mid-volume ETFs, market makers may purchase a small position back Market-On-Open (MOO) rather than creating a larger position. Other dealers recognize this and will price MOO orders with larger premiums.

At the market close…

At market close, liquidity decreases, and market makers face hedging and balance sheet constraints. Large Market-On-Close (MOC) trades can distort ETF pricing. Executing trades in the last 10 minutes of the session, rather than exactly at the close, can reduce price impact.

Into the Close, NOT on the Close

ETF prices reflect the value of the underlying holdings, as well as the costs of carrying and hedging risk. At 4:00 pm EST, the market maker cannot reduce its position through creation/redemption; thus, it will charge the highest carry cost. Additionally, the cost to offset the risk of the ETF trade is significantly higher, as the equity market has closed and liquidity in the futures market is lower. Executing over the last 10 minutes of the day would have considerably reduced the price impact.

MOC Dislocation…even for the most liquid traded instrument in the world

Use Limit Orders

Limit orders help control execution prices and mitigate the risk of unfavorable fills.

The Plus and Minus

- Positive: You can never receive worse execution than your limit, and you can find price improvement.

- Negative: While limit orders guarantee price protection, execution is not assured if other orders have time precedence or are executed on different venues.

Suggested Limit Price strategy:

- When purchasing ETF shares, place a limit price a few pennies above the offer.

- If the offer price is $50.00, use $50.02 as the limit buy price.

- When selling ETF shares, place a limit price a few pennies below the bid price:

- If the bid price is $50.00, use $49.98 as the limit sell price.

This strategy does not guarantee execution, but it is likely to enhance the chances of a successful outcome.

Worst-Case Scenario

Be Cautious Around Events/News

- Market-moving news increases volatility.

- Volatility reduces dealer commitment and widens spreads.

- In the volatile markets, executions become more difficult and less predictable.

Beware the Ides of March…or at least market-moving news

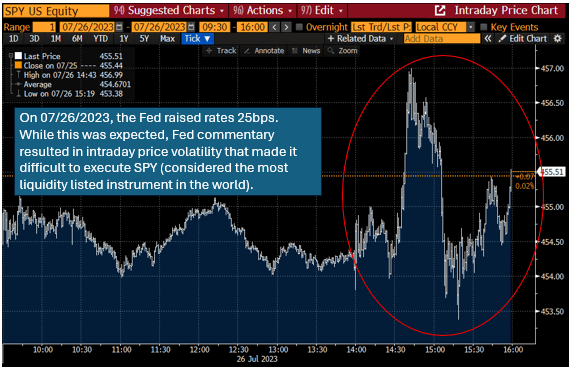

When markets experience increased volatility due to events or news, the cost of offsetting risk rises dramatically. This forces market makers to widen quotes and reduce available liquidity. Market prices can fluctuate significantly as new information is digested and expected outcomes shift. Below is a graph that represents a 2:00 p.m. ET rate hike that was expected and had a limited impact. Thirty minutes later, the Fed’s commentary surprised the market, and the price movement reflected this surprise.

Markets Rise, Markets Fall… sometimes very quickly

Beyond DIY

Using a Centralized Trading Desk

Centralized trading desks have well-established direct connectivity to ETF market makers, enabling access to deeper pools of liquidity across asset classes, regardless of market conditions. To maximize effectiveness, placing Not-Held orders provides centralized trading desks with the greatest flexibility in managing specific orders.

What’s a Not-Held Order Type?

The Nasdaq defines a not-held order type as a market or limit order in which the customer does not wish to transact automatically at the inside market (market held) but instead has given the trader or floor broker (listed stock) time and price discretion to transact on a best-efforts basis.

Not-Held orders give trading desks discretion over execution, which is especially useful for lower-volume ETFs or during volatile market periods. When accepting a “Not-Held” order, centralized trading desks assume a fiduciary responsibility to their clients and manage the order accordingly.

To navigate this environment successfully, investors must look beyond surface-level quotes and engage with the deeper layers of liquidity that are available. By leveraging centralized trading desks and using Not-Held order types, investors can more easily access, indirectly, these deeper pools of liquidity.

Opening the lines of communication

The ETF market-making community operates in a highly competitive environment. Three key pieces of information enable ETF market makers to provide on-demand liquidity requests for block trades and minimize the impact of trade execution:

- Insight into the expected time frame for the order helps market makers prepare effectively.

- Understanding the expected order size allows ETF dealers to properly set electronic quotes and adjust any limitations on risk parameters for on-demand block trades.

- Knowing the order’s origin is significant. When the source is a genuine investor rather than a hedge fund or “fast money” entity seeking to exploit market makers, ETF dealers are more comfortable trading in a highly competitive mode.

Sharing order size, timing, and origin helps market makers optimize quotes and manage risk, improving execution quality. Capital markets teams play a key role in facilitating this communication.

The Takeaway

To achieve optimal ETF trade execution:

- Avoid trading at market open or on the market close

- Use limit orders to cap potential unfavorable and avoidable poor price executions.

- Assess market conditions before executing trades, especially during periods of heightened volatility or low liquidity.

- For large or complex trades, utilize centralized trading desks and “Not-Held” order types to access deeper liquidity and minimize market impact.

- Transparent communication regarding order size, timing, and origin enables market makers to provide better quotes and manage risk effectively.

Related Content

More Insights

Real Estate Market Recap: Trends, Challenges, and What Comes Next

Beyond the Hype—Building Smarter Private Credit Portfolios

Structural Forces Are Driving the Current Investment Environment

Finding Opportunity Amid Imbalance: 2026 Market Outlook

Thornburg Income Builder Opportunities Trust Announces Distribution