As an advisor, it’s in everyone’s best interest to help clients actively manage their legacy wealth.

The old adage “from shirtsleeves to shirtsleeves in three generations” describes the challenge of sustaining family wealth. While it always makes sense to take adages with a grain of salt, this one actually warrants our attention because a 2015 U.S. Trust survey of high-net-worth investors (defined as individuals with over $3 million in investable assets) found that, by the second generation, 70% of family wealth is lost and, by the third generation, 90% has evaporated.

We’ve seen it in the movies and with people we know, wealthy families who at one point had everything—money, prestige, and power—lost it all through a series of missteps and wound up with little or no wealth left to pass on to future generations. While this “riches to rags” phenomenon may not have interested you in the past, today it warrants your laser focus because it speaks to an occurrence that could spark some significant growth in your business: generational wealth transfer.

The Changing Face of the Financial Services Industry

There’s no question that a financial advisory career is attractive. Challenging and energizing, this is a business where you can earn a great living, be your own boss, and actually measure the relationship between your efforts and success.

Like our ever-changing world, the financial services industry is dynamic and never boring. The fast pace and the challenge of navigating clients through volatile markets keep you engaged and interested. But while your interest in and passion for this business are critical prerequisites for success, over the long term your success in this industry actually depends upon your ability to anticipate and adapt to generational change.

Today’s financial services industry doesn’t resemble that of 20, 10, or even five years ago. To remain relevant, we matured, embraced technology and evolved with the times. Now we’re at an inflection point. Created by changing demographic trends such as longevity and generational wealth transfer and industry trends like competition from online, algorithm-driven portfolio managers and increased regulatory scrutiny, you’re being forced to make changes today to remain in business tomorrow.

Today’s Best Business-Building Opportunity—Managing Legacy Wealth

In this business the best opportunities are always found where money movement and consumer needs intersect. For the foreseeable future, you will find those opportunities where there is intergenerational wealth transfer.

Is this Great American Wealth Transfer really significant? Take a look at some of the numbers:

- According to a 2015 State Street Global Advisors’ survey, “Money in Motion” ( June 2015), $2 trillion is expected to change hands between 2012 and 2017.

- Accenture’s 2012 white paper, “The ‘Greater’ Wealth Transfer: Capitalizing on the Intergenerational Shift in Wealth,” reported that between 2011 and 2048, baby boomers are expected to transfer $30 to $41 trillion to Generation X and Millennials.

- Diane Doolin, co-founder of the Institute for Preparing Heirs, tells us that as many as 20,000 estates worth more than $20 million each are transferred each year. For financial advisors, this means that the risk of losing assets and the opportunity of gathering additional assets is greater than it’s ever been.

This transfer of wealth between generations represents a once-in-a-lifetime business-building opportunity, not just because of the amount of money that’s being transferred but because once the money is transferred, research tells us that the heirs will likely move the money to different advisors.

According to a 2013 PriceWaterhouseCoopers Global Private Banking/Wealth survey, when parents die only 2% of heirs leave their money with their parents’ financial advisor. This means that 98% of their heirs move their money to their existing advisor or they choose a new one. Your challenge is to ensure you’re an advisor who keeps your clients’ heirs money and the one who captures assets from other advisors’ clients’ heirs. Becoming a legacy wealth manager is a great way to achieve that goal.

Managing Legacy Wealth

Historically, financial advisors have done a great job of providing clients with investment management strategies geared toward asset accumulation. At some point, clients’ goals change and they shift their interest from asset accumulation to wealth distribution and transfer. When that happens, they expect their advisor to tell them how to establish goals and craft a plan for identifying and managing the wealth they want to transfer to their heirs. Surprisingly, the wealth they want to transfer is not always tangible.

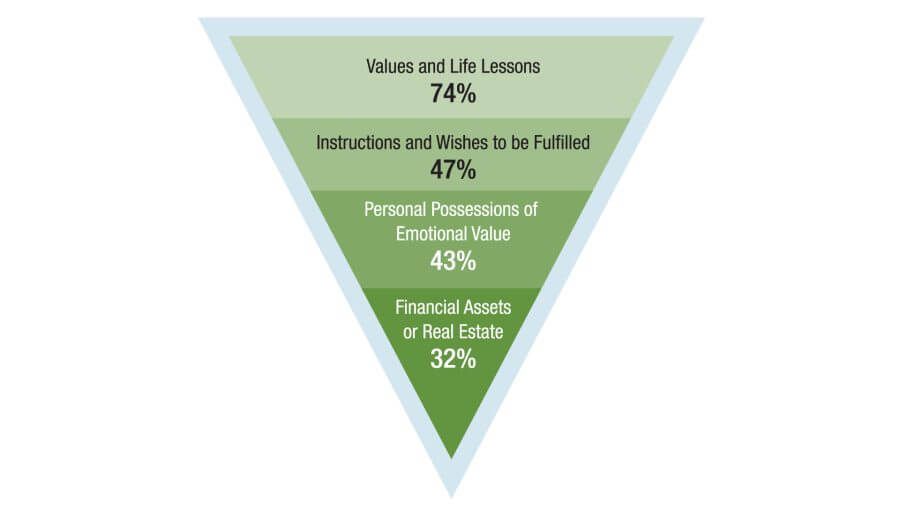

According to “The Four Pillars of Legacy” from Age Wave, “the world’s leader in understanding the effects of an aging population on the marketplace,” there are four critical “possessions” individuals want to pass on to their heirs. In descending order of importance, Age Wave found that 74% want to pass on values and life lessons, 47% want their instructions and wishes to be fulfilled, 43% want to pass on personal possessions of emotional value, and 32% are interested in passing on financial assets or real estate.

What Clients Want to Pass on

Source: Age Wave, “The Four Pillars of Legacy”

Source: Age Wave, “The Four Pillars of Legacy”

Instead of looking for an expert in just transferring tangible property like possessions, securities, and real estate, today’s high-net-worth (HNW) clients want a financial advisor who has the expertise to manage their investments, understands the importance of passing along family values, and has the experience to lead the entire family through a legacy wealth management process that can often be challenging.

Becoming a Legacy Wealth Manager

As with any evolution of a business, financial advisors who become legacy wealth managers climb a steep and fascinating learning curve as they increase their expertise, knowledge, and skills including:

- Developing a diverse, multi-generational team of advisors.

- Understanding the characteristics, needs, and differences between generations.

- Defining the needs of HNW clients and developing a legacy wealth management and client service process to address the HNW clients’ needs.

- Becoming an expert in leading families through a process that helps them agree upon their family mission, goals, and governance process.

Family wealth that is built over decades can be destroyed in a heartbeat. For HNW families, a financial advisor’s expertise and guidance is often the only thing protecting the family elders and their current and future heirs from making inappropriate or ill-conceived financial decisions that could destroy their family’s wealth.

Going forward, increased competition and lower revenues may force you to acquire more clients and assets just to maintain your current production levels. But as a financial advisor, you are a member of a community of high-achievers who are not content to “stand in place”. You want to move forward and grow your business. To grow your business, consider reinventing your advisory practice and repositioning yourself and your team as legacy wealth managers who understand the challenges of wealth transfer and have a process for solving the problems of prospects and clients who are interested in ensuring their family wealth benefits current and future generations.

Discover more about:

More Insights

Tariffs, Stagflation, and the Fed: A Spotlight on Investors’ Most Pressing Questions

How We Invest: Active by Nature. Disciplined by Design.

Thornburg Income Builder Opportunities Trust Announces Distribution

Investment Perspectives from the Road: The UAE

Investor Update: A Potential Reprieve for the Municipal Bond Tax Exemption