The investment landscape is shifting from the past decade of focusing on capital appreciation and de-emphasizing dividend income.

Why Dividends Now?

The current financial backdrop is notably different from the post-Great Financial Crisis era. Central bank balance sheets, which have ballooned over the last 15 years, and a long period of near-zero interest rates, have created distortions in asset prices. With a return to more traditional interest rate levels, investors need to adapt to this new paradigm.

Higher Rates Favors Companies That Are Better Stewards of Capital

One key opportunity in this environment is dividend-paying stocks. Historically, dividend-paying strategies have not only delivered higher total returns but have also done so with less volatility. For example, over the past 50 years, dividend-paying stocks have returned an average of 9.12% annually, compared to just 4.19% for non-dividend-paying stocks. This demonstrates the long-term benefits of dividends as a cornerstone of total return.

Companies That Can Grow Their Dividend Have Historically Outperformed

Dividends as an Inflation Hedge

In addition to providing income, dividends have historically acted as an inflation hedge. Since the 1940s, dividend growth has typically outpaced inflation, providing investors with inflation-protected income. This is especially relevant today as investors seek protection from the recent surge in inflation.

Dividends are an Effective Hedge Against Inflation

The Yield vs. Growth Dynamic

When assessing dividend-paying stocks, it’s important to differentiate between yield and dividend growth. While the current dividend yield on the market may be lower than in previous periods, dividends per share have continued to grow rapidly. This means that even if yields appear lower, the actual income investors receive can increase significantly over time, creating a powerful compounding effect.

Moreover, dividend-paying stocks are currently trading at attractive valuation levels, particularly in comparison to growth stocks. Historically, dividend stocks have traded at a 10-20% discount to growth stocks due to their lower growth expectations. However, today that discount has widened to 52%, suggesting significant potential for dividend stocks to appreciate relative to growth stocks.

Income-Generating Equities Present Attractive Value

Source: Bloomberg as of 30 June 2024.The Global Dividend Opportunity

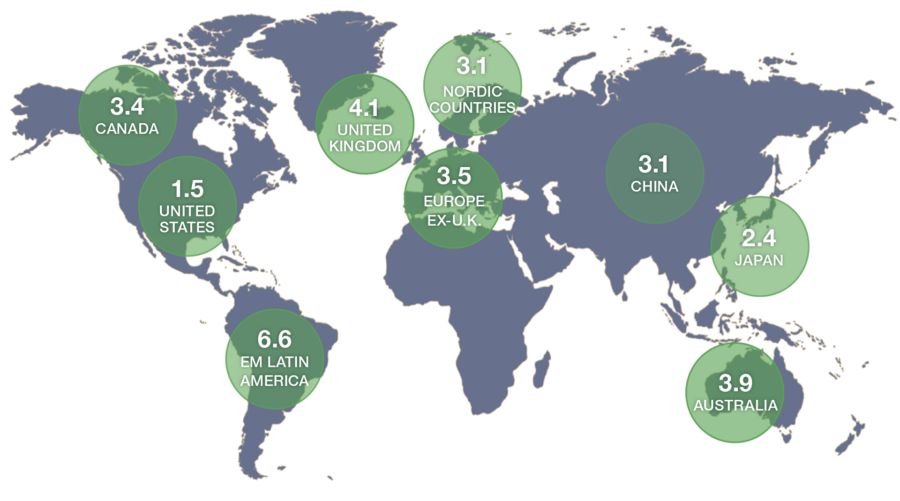

Looking beyond the U.S., international markets present additional opportunities for dividend investors. The U.S. market has one of the lowest dividend yields in the world at just 1.5%, compared to higher yields in regions like Europe, the UK, and Australia. Diversifying globally allows investors to access higher yields and greater diversification, which can enhance the overall resilience of a portfolio.

Non-U.S. Equity Markets Have Better Opportunities for Income

Furthermore, the past 15 years have seen international markets underperform compared to U.S. markets, largely due to unusual monetary policy. As we transition to a more normalized policy environment, international markets may outperform in the coming years, making them an attractive area for dividend-focused investors.

The Role of Dividends in Total Return

Dividends have historically played a significant role in total return, accounting for nearly 50% of total returns over longer time periods. While the past decade has seen dividends contribute a smaller portion of total return, their long-term significance remains unchanged. For investors seeking a balanced approach to income and capital appreciation, dividends are a crucial component of portfolio strategy.

Historically, Dividends Have Been Essential to Total Return

In today’s uncertain environment, dividend-paying strategies offer a compelling combination of income, inflation protection, and long-term growth potential. Investors would be well-served to revisit the role of dividends in their portfolios as they seek to build resilience and capitalize on opportunities in the evolving market landscape.

Discover more about:

Related Content

More Insights

Tariffs, Stagflation, and the Fed: A Spotlight on Investors’ Most Pressing Questions

How We Invest: Active by Nature. Disciplined by Design.

Thornburg Income Builder Opportunities Trust Announces Distribution

Investment Perspectives from the Road: The UAE

Investor Update: A Potential Reprieve for the Municipal Bond Tax Exemption