If You Have Long-Term Goals, You Must Think Long-Term.

“It’s not timing the market, it’s time in the market that matters.” —Financial services industry adage

After years of education, decades of experience, and a lifetime of insight and perspective, Jeremy Siegel, the Russell E. Palmer Professor of Finance at the Wharton School of the University of Pennsylvania and author of the 1994 book, Stocks for the Long Run, needed just five words to summarize, as the quote indicates, what wise investors have always known: investing is a long-term proposition.

Unlike bonds, which represent a debt of the issuing company, shares of stock represent ownership, or equity in the issuing company. When an investor buys a bond, she knows that the company will compensate her with regular interest payments, in return for the use of her money. Those who invest in stock do so with the hope that as a company becomes successful, the company’s stock will appreciate in price and shareholders will see their investment increase in value.

Studies have shown that the individuals who earn the best investment returns—despite economic changes and market fluctuations– are investors who buy stock and remain invested for the long term. While most investors know intellectually that investing in stock is a long-term proposition, emotionally they want an instant winner. If they don’t get one, they’ll move on to the next opportunity. That short-term, hit-and-run thinking negatively affects investor returns and we have the numbers to prove it.

For more than 25 years, Dalbar, a financial services market research firm, has studied investor behavior and success by comparing individual investors’ performance to investment market performance. Dalbar’s studies have demonstrate, time and time again that individual investors earn less than investment indices.

One Dalbar study for the time period ending in 2013, compared investors’ returnsto the returns of the S&P 500 Index. In the study they discovered that between 1983 and 2013, the S&P 500 returned an average 11.1% per year while, over the same time period, the typical stock mutual fund investor earned an average of 3.69% per year. Of the difference, Dalbar attributed 1.4% to mutual fund expenses and the rest to investors’ poor timing decisions. But how do we know that short-term thinking is negatively affecting investor returns?

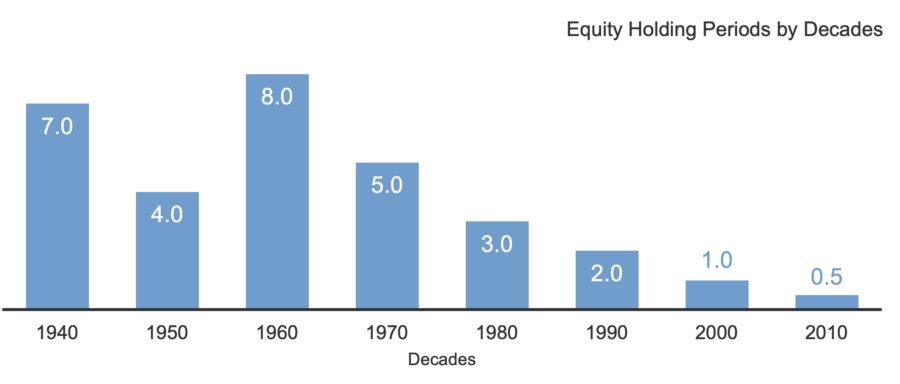

This chart from Dr. Daniel Crosby’s book, The Laws of Wealth: Psychology and the Secrets to Success demonstrates, that on balance, equity investment holding periods since the 1940s have generally declined. Specifically, compare the 8-year average holding periods of the 1960s to the 2010s when investor holding periods averaged just 5 months.

Three ways investors can avoid falling into the short-term investor mindset:

- Work with a financial advisor who understands you and your life goals. Increases in life expectancy require investors to have financial and investment plans that assume they will live until age 100, which means that some of us may be retired for 30 or 40 years. In addition to focusing on your goals, your advisor will recommend investment strategies and securities that fit your needs.

- Become a student of stock market history (just a student, not a professor). Compare short-term (1-5 years) market performance to long-term performance (5+ years). Notice that, while markets can fluctuate dramatically over a one- or two-year period, those dramatic fluctuations become small hiccups when you consider longer time periods

- Avoid looking at your investment accounts every day, because what you see on any given day may cause you to take unnecessary action like selling a security. Greg Davies, the head of Behavioral Finance at Oxford University studied investment account values and found that if an investor looks at her account values every day, 41% of the time she will see they are down in value; the investor who looks at their accounts every 5 years will see their account is down 12% of the time; and the investor who looks at their account every 20 years will never see they have lost money.

When Jeremy Siegel titled his book, Stocks for the Long Run, he gave us the answer to investor success. But his book’s title didn’t explain the critical role financial advisors play in ensuring that the habit of long-term investing is widely adopted.

Discover more about:

Related Content

More Insights

How We Invest: Active by Nature. Disciplined by Design.

Thornburg Income Builder Opportunities Trust Announces Distribution

Investment Perspectives from the Road: The UAE

Investor Update: A Potential Reprieve for the Municipal Bond Tax Exemption

Thornburg Investment Income Builder Fund – 2nd Quarter Update 2025