Some argue that over time emerging markets will converge with developed markets and dampen risk. Perhaps. But which developed market is your benchmark?

As emerging markets investors, we admit to being positively biased toward the region. Our positive feelings towards the asset class feel justified when we listen to earnings calls of Western corporations continually point to emerging markets as drivers of their future growth. After all, there is much to be excited about when it comes to emerging markets as the region enjoys multiple structural tailwinds: attractive demographics, urbanization, technological advancements, low penetration of consumer/financial products, and more.

While developed market firms are excited about the growth potential in EM, investors are more cautious and view EM as more risky and volatile. One question we often hear is: when will emerging markets converge to developed markets (“convergence theory”)? The implication is that when emerging markets mature and resemble developed markets, the risks of investing there will fall.

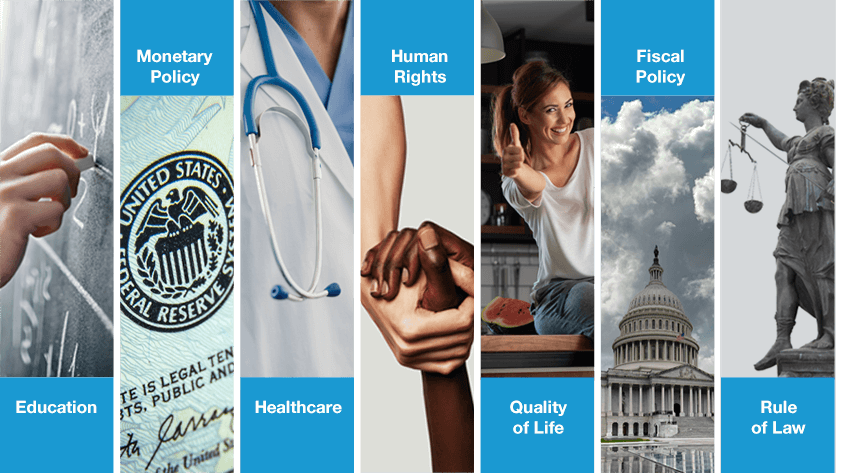

We dug further into the convergence theory by evaluating emerging and developed markets across various metrics: the rule of law, human rights, access to healthcare and education, monetary and fiscal policies, technology penetration, and quality of life.

Defining terms: What Does Convergence Mean?

After our due diligence, we determined that this theory is fundamentally flawed, and the flaw is most starkly exposed when reviewing developed markets. DM countries’ performance against these metrics has fluctuated over time, yet those fluctuations do not seem to impact or influence DM equity markets returns over the long term.

Rather than benchmarking emerging markets to developed, we believe that all countries should be benchmarked to an “ideal” investing environment. For us, the United States between 1980-2020 is an excellent example of this “Goldilocks” phenomenon.

“Goldilocks” Investing Environment

Between 1980 and 2020, the United States enjoyed remarkable growth. At a very high level, two key drivers for that outperformance were (1) the rise of the middle class and (2) falling interest rates.

-

Rise of U.S. Middle Class

Per the U.S. Census Bureau, the percentage of Americans earning $50,000 or more rose from ~24% of the total population in 1980 to ~39% in 2020 (income figures adjusted for 2021 dollars). The rise of the middle class was propelled by multiple factors: globalization, technological advancements, financialization, and improved access to credit and pro-growth government policies.

As American prosperity rose, a positive feedback loop formed. With higher disposable income levels, American consumers had more resources to spend on goods and services. This surge in consumer spending, in turn, stimulated further economic growth and created fresh investment opportunities.

-

Falling Interest Rates

Another significant driver behind investment gains in the United States has been the decline in interest rates. From 1980 to 2020, the Federal Funds rate dropped from over 14% to approximately 1.5%. Low interest rates made it easier for businesses to borrow money to fund their operations and consumers to borrow and purchase homes that provided another source of savings (outside the Global Financial Crisis years).

This trend was particularly notable in the 2010s following the Global Financial Crisis, as interest rates remained near zero for a significant portion of the decade resulting in a surge of liquidity in the U.S. financial markets. Entrepreneurs and the U.S. tech sector significantly benefited from this liquidity influx. The lower cost of capital made it easier for new start-ups to secure funding through lending and initial public offerings. As a result, many were rewarded for prioritizing innovation and market share growth over profitability.

The Goldilocks Scenario: The U.S. From the 1980s Onwards

Rise of the U.S. Middle Class

Falling Cost of Capital and Inflation

U.S. Equity Performance

Source: Pew Research Center, Bloomberg

Today’s Emerging Markets Bear Strikingly Similar Characteristics to This “Goldilocks” Scenario

In 2009, less than half of the global middle class resided in emerging markets (approximately 46%). Globalization catalyzed the expansion of EM’s middle class through increased trade, foreign direct investment, the establishment of new industries, and the creation of higher-value jobs. By 2020, over 70% of the global middle class was concentrated in emerging market countries, and this cohort is potentially projected to reach 80% by 2030.

This trend highlights an important nuance. Previous bullish arguments for emerging markets as an asset class primarily focused on the sheer population size of the region, known as the demographic dividend theory. However, we now recognize that population growth alone cannot drive economic development. People also require disposable income to fuel consumption. We believe that emerging markets have passed this tipping point. The emerging markets’ middle class has the numbers (meaning it has reached critical mass as a proportion of the overall population) and the money to drive structural economic growth.

Middle Class Populations Are Surging, Led by Emerging Markets

Global Middle Class – Population (bln)

Emerging Markets as a Percentage of the Global Population

Source: World Bank, Wolfensohn Center for Development at the Brookings Institute

-

Falling Interest Rates

Emerging markets learned valuable takeaways from past financial crises that occurred 30-40 years ago, such as the Latin American Debt Crisis, the Mexican Peso Crisis, and the Asian Financial Crisis. These disruptions were marked by substantial depreciations in exchange rates, which destabilized both local economies and undermined faith in the central bankers that oversaw monetary policies.

-

- In the 1980s, Latin American countries borrowed from U.S. banks at manageable rates. However, when the U.S. Federal Reserve began raising interest rates, these countries were overburdened by their debt obligations.

- Both the Mexican Peso Crisis and the Asian Financial Crisis centered around the devaluation of currencies. A combination of market factors, including the influx of speculative funds, made it challenging for emerging market countries to maintain their local currency pegs to the U.S. dollar. When these governments were eventually forced to allow their currencies to float, they experienced significant devaluations. For instance, the Mexican peso depreciated by 50% in just four months, while Asian currencies faced similar turmoil between 1997-1998.

After surviving these crises, emerging markets learned the importance of controlling their individual monetary policies. Not only is it vital to effectively navigate economic challenges, but monetary authority enables central bankers to earn and build credibility within the global investment community.

Keeping these lessons in mind, over the past two decades, central banks in emerging markets have followed orthodox monetary policies and maintained relatively high policy rates. They remained steadfast in their approach, even during the recent pandemic when accommodative monetary policies appeared justifiable. That left emerging markets central banks ahead of their developed market counterparts. As a result, inflation in these markets rose modestly compared to historical trends, and real interest rates remained positive across several major emerging economies.

Thanks to their central banks’ monetary discipline, emerging markets are now positioned to ease earlier than developed markets. Monetary stability and declining interest rates provide an attractive backdrop for emerging markets equities. Lower policy rates will benefit emerging market corporations as their cost of capital will also fall, thus improving their bottom line.

Emerging Markets Policy Rates Are Poised to Decline

Regional Policy Rates and Inflation

Regional Real Rates

Source: Bloomberg

It’s interesting to note that a significant advantage enjoyed by developed markets corporates is gone and may never be restored. Throughout the 2010s, developed market companies secured loans at much lower rates compared to their emerging markets counterparts. However, inflation may now be higher for longer from here, due to factors such as deglobalization and concerns about national security related to supply chains, which means that policy rates may also now be higher for longer.

As a consequence, an entire generation of business leaders who have only operated in a low-interest rate environment must adapt and relearn how to effectively manage their businesses. Let’s be honest – not all companies will be able to keep up with the changing times.

Emerging Markets: The Opportunity for Active Management

Convergence theory remains a valuable tool for assessing investment opportunities in both emerging and developed markets when the benchmark is updated for an “ideal” investment environment rather than comparing the regions directly. From our perspective, the investment landscape favors emerging markets, thanks to the growth of their middle class and the easing policy rate cycle. (And don’t forget the added advantage EM corporates have from their knowledge of operating in high-cost-of-capital environments.) We believe that strong businesses with high-quality growth prospects will thrive.

Discover more about:

More Insights

Thornburg Income Builder Opportunities Trust Announces Distribution

Navigating Tight Credit Spreads With a Defensive Income Mindset

Equity Income Builder Fund Update: Staying Grounded in Fundamentals

Thornburg Income Builder Opportunities Trust Announces Distribution

Beyond the Benchmark: Finding Global Opportunities